The following performance numbers are being reported publicly for HANA:

HANA scans data at 3MB/msec/core

On a high-end 80-core server this translates to 240GB/sec per node

HANA inserts rows at 1.5M records/sec/core

Or 120M records/sec per node…

Aggregates 12M records/sec/core

Or 960M records per node…

These numbers seem reasonable:

A 100X improvement over disk-based scan (The recent EMC DCA announcement claimed 2.4GB/sec per node for Greenplum)…

Sort of standard OLTP insert speeds for a big server…

Huge performance gains for in-memory aggregation using columnar orientation and SIMD HPC instructions…

Note that these numbers are the basis for suggesting that there is a new low-TCO approach to BI that eliminates aggregate tables, materialized views, cubes, and indexes… and eliminates the operational overhead of computing these artifacts… and still provides a sub-second response for all queries.

I want to soften my criticism of Greenplum‘s announcement of HAWQ a little. This post by Merv Adrian convinced me that part of by blog here looked at the issue of whether HAWQ is Hadoop too simply. I could outline a long chain of logic that shows the difficulty in making a rule for what is Hadoop and what is not (simply: MapR is Hadoop and commercial… Hadapt is Hadoop and uses a non-standard file format… so what is the rule?). But it is not really important… and I did not help my readers by getting sucked into the debate. It is not important whether Greenplum is Hadoop or not… whether they have committers or not. They are surely in the game and when other companies start treating them as competitors by calling them out (here) it proves that this is so.

It is not important, really, whether they have 5 developers or 300 on “Hadoop”. They may have been over-zealous in marketing this… but they were trying to impress us all with their commitment to Hadoop… and they succeeded… we should not doubt that they are “all-in”.

This leaves my concern discussed here over the technical sense in deploying Greenplum on HDFS as HAWQ… or deploying Greenplum in native mode with the UAP Hadoop integration features which include all of the same functionality as HAWQ… and 2x-3X better performance.

It leaves my concern that their open source competition more-or-less matches them in performance when queries are run against non-proprietary, native Hadoop, data structures… and my concerns that the community will match their performance very soon in every respect.

It is worth highlighting the value of HAWQ’s very nearly complete support for the SQL standard against native Hadoop data structures. This differentiates them. Building out the SQL dialect is not a hard technical problem these days. I predict that there will be very nearly complete support for SQL in an open source offering in the next 18-24 months.

These technical issues leave me concerned with the viability of Greenplum in the market. But there are two ways to look at the EMC Pivotal Initiative: it could be a cloud play… in which case Greenplum will be an uncomfortable fit; or it could be an open source play… in which case, here comes the wacky idea, Greenplum could be open-sourced along side Cloud Foundry and then this whole issue on committers and Hadoopiness becomes moot. Greenplum is, after all, Postgres under the covers.

English: In visible light, 4C 71.07 is less than impressive, just a distant speck of light. It’s in radio and in X-rays – and now, gamma rays – that this object really shines. (Photo credit: Wikipedia)

The shared-nothing architecture has, from the beginning, offered the promise of using hardware to solve performance problems rather than applying staff and tuning. By this I mean… if you can add nodes and scale out to improve query response then why not throw hardware at performance problems rather than build a fragile infrastructure of aggregate tables, cubes, pre-joined/de-normalized marts, materialized views, indexes, etc. Each of these performance workarounds are both expensive to build and expensive to operate.

There are several reasons, I think tuning has been more popular than scaling. Not in any particular order:

First, hardware vendors made it too hard to order/provision new nodes. You could not just press a button and buy capacity. Vendors wanted to charge you for terabytes when all you wanted might be CPU and Memory to fix the problem (see here, sigh). You had to negotiate a deal with a rep, work through your procurement group, wait weeks for delivery. Then, the hardware you have might not match the hardware for sale. New models could not be mixed with old nodes… so you had to consider a whole new cluster. The process was so not-agile. There have been attempts to fix this… and some of them are credible… but none are popular.

Next, the process to install the new nodes was moderately difficult… not rocket science but not seamless to be sure. Data had to move. Backups had to be reconfigured and sometimes old backups could not be easily restored to the new configuration. There was no easy way to burn in the new hardware and if it failed early there were issues reversing the process. It just was not considered an everyday operational process… it was the exception and that made it tough. This process too has improved over time but it never became a no-brainer.

Finally, buying hardware is a capital expense (CAPEX). Even if you had to pay more in people costs to do the hard work of tuning those were operational expenses… and funding was easier to get.

Redshift changes the game here. Even if the Paraccel database is just OK (see here)… and if the overhead of running in the virtualized AWS environment makes it worse… it is still OK. You can provision new hardware in a couple of minutes. If Teradata is 25% faster than Paraccel for your query set… so what? You can add 25% more Redshift for a fraction of the extra cost of Teradata. Need more performance? Dial it in. Need permission? No problem because it is all OPEX dollars.

Redshift will deliver the flexibility to make scale out less expensive than tune it out. The TCO reductions from running a simple system where hardware solves performance problems instead of ETL and staff will be significant. This is how it always should have been.

The issue for Redshift will be… given the trend to reduce the data latency from operations to BI… can you move significant amounts of data from on-premise into the cloud fast enough to meet service level agreements?

Do not overlook Redshift… Amazon could be a player in the EDW space… But look for other databases to make inroads here as well. In-memory databases could work well in the cloud as they avoid some of the hardware abstraction required to access disks.

If Greenplum HAWQ does not look promising (see my previous posts on HAWQ here and here) what are the prospects for TeradataAster Data… which aspires to both replace and/or co-exist with Hadoop for a fee? Teradata+Hadoop maybe… but Teradata+Aster+Hadoop seems like one layer too many… as does Aster+Hadoop.

(OK, I removed the bad “HAWQing” pun in the title… no complaints from readers… it just seemed unfair… – Rob)

My contacts from Strata read my post here and provided me with the following information:

The performance numbers quoted for Greenplum HAWQ versus HIVE and Impala used Greenplum tables implemented over HDFS. In other words, this data is unreadable from outside of the Greenplum database… unreadable by any other program in the Hadoop eco-system… a proprietary format. If the tests were re-run using the same open data structures used by HIVE and Impala you would find the performance of HAWQ to be closer to, or worse than, those Hadoop components.

The HAWQ performance numbers quoted represent a 2X-3X performance degradation over the same benchmark run on the native Greenplum RDBMS.

Again… this is from a credible source… but please consider this a rumor… and view this report, and the associated Greenplum marketing… with an appropriate measure of engineering skepticism.

Greenplum is a fantastic product… if I assume the report to be true then I do not understand why are they doing this… what use case is solved by a 300% performance degradation accessing proprietary data in HDFS? Remember, you could put Greenplum in the same cluster as Hadoop (UAP) and query everything HAWQ could query without the performance degradation. I just do not see the point? Could someone from GP comment and help my readers and myself here?

First, from a technical standpoint I like the Greenplum-on-HDFS HAWQ offering. It looks like the GP Team replaced XFS with HDFS and added some native support for several HDFS file types. I will say more on this soon.

But I would like to weigh-in on the question raised by HortonWorks here… is HAWQ Hadoop? And I have a question towards the end…

Let me propose an analogy: Hadoop is an eco-system of open source components much like LINUX is an eco-system of open source components. If you think the analogy apt, then HAWQ on HDFS is not Hadoop any more than Microsoft Internet Explorer on LINUX is LINUX. Hive is open source and part of the Hadoop eco-system… as is Impala. Firefox is open source and part of the LINUX eco-system. HAWQ is not Hadoop.

The HortonWorks link points out that Greenplum is not engaged in the Hadoop eco-system as a contributor. They also quote Greenplum as saying that they have 300 developers working on Hadoop. Well… if HAWQ is part of Hadoop and HAWQ is the Greenplum database on HDFS then they have 300 developers on Hadoop. But if, as I suggested, HAWQ is not Hadoop then the number of Greenplum developers on Hadoop might be less. I bumped into a long-time Greenplum employee at Strata who told me that HAWQ was a skunkworks project with 4-5 developers max. This comes from a credible source… but it is still rumor-quality… so take it with a grain of salt.

The bottom line is that Greenplum has marketed very aggressively. They fuzz the definition of Hadoop to claim their commercial database offering running on Hadoop is therefore “Hadoop”. They fuzz the definition of developers working on Hadoop based on this first fuzz.

But does it matter? Greenplum will read and process data stored in HDFS faster than any other SQL-based engine. That is worth something.

But what is it worth? I’m fairly certain that the Greenplum databases will run faster off of Hadoop on XFS than in Hadoop… maybe significantly faster. So the reason for Greenplum on HDFS is faster SQL access to data in HDFS files.

This leads me to my question. I wonder… were the performance numbers quoted, showing a significant performance advantage over both HIVE and Impala, based on queries executed against the Greenplum proprietary table formats or against the same native HDFS file types read by HIVE? If they ran against Greenplum tables then I wonder what the real apples-to-apples comparison would show? Note that I am not being cynical here… I do not know how the tests were set up… only that Greenplum was fast. But if as I said: ” the reason for Greenplum on HDFS is faster SQL access to data in HDFS files” and the data was in Greenplum file structures accessible only by Greenplum then there is little reason left.

I also wonder if it matters because HIVE and Impala will improve their performance significantly over the next 12-24 months. The sheer amount of human R&D being expended here will allow these SQL engines to catch, or nearly catch, HAWQ in performance. If there is any gap left, the price and the community of open source offerings will defeat HAWQ in the market.

As I have suggested here… there is no apparent commercial opportunity competing against Hadoop at this point. I suggested here that Hadoop would eat Greenplum if they stuck to the analytics space and offered both products… effectively competing with themselves. This new strategy is not likely to work in the medium or long run. Greenplum is, indeed, all-in on Hadoop… but without a winning hand.

March 10: See here for the answers to my questions… – Rob

March 12: See here for a rethink on this subject… – Rob

Vertica is the product I saw the most. In fact before they were acquired they were beginning to pop up a lot. The product is innovative in several dimensions. It is wholly column-oriented with several advanced columnar optimizations. Vertica has an advanced data loading strategy that quickly commits data and then creates the column orientation in the background. This greatly reduces the load time but slows queries while the tuples are transformed from rows to columns. Vertica offers a physical construct called a projection that may be built to greatly speed up query performance. Further, they provide a very sophisticated design workbench that will automatically generate projections.

Paraccel is the company I saw the least. I never saw it win… but I know that it does, in fact, win here and there. My impression, and I use this fuzzy word intentionally as I just don’t know, is that Paraccel is a solid product but it does not possess any fundamental architectural advantages that would allow it to win big. Every product will find an acorn now and again. The question is whether in a POC with the full array of competitors there is a large enough sweet spot to be commercially successful? I think that Paraccel cannot win consistently against the full array. Paraccel is now the basis for the Amazon Redshift data warehouse as a service offering. This will keep the product in the game for a while even if the revenues from a subscription model do not help the business much.

Where They Win

Vertica wins when projections are used for most queries. They are not likely to win without projections. This makes them a very effective platform for a single application data mart with a few queries that require fast performance… or for a data mart where the users tend to submit queries that fit into a small number of projection “grooves”.

Paraccel wins in the cloud based on Redshift. They can win based on price. They win now and again when the problem hits their sweet spot. They win when they compete against a small number of vendors (which increases their sweet spot).

Where They Lose

Vertica loses in data warehouse applications where queries cut across the data in so many ways that you cannot build enough projections. Remember that projections are physical constructs with redundant data.

Paraccel loses on application-specific marts and other data marts when the problems fit either Vertica’s projections or Netezza’s zone maps. They lose data warehouse deals to both Teradata and Greenplum when the query set is very broad. They will lose in Redshift when performance is the key… maybe. I have always thought that shared-nothing vendors made it too hard and too expensive to scale out. It should always have been easier to add hardware to improve performance than to apply people to tuning… but this has not been the case… maybe now it is (see here)?

In the Market

Since the HP acquisition the number of times Vertica shows up as a competitor has actually dropped. I cannot explain this but HP has had a difficult time becoming a player in the data warehouse space and had several false starts (Neoview, Exadata, …). The product is sound and I hope that HP figures this out… but HP is primarily a server vendor and it will be difficult for them to sell Vertica and stay agnostic enough to also sell HANA, Oracle, Greenplum, and others.

The Amazon Redshift deal breathes life into Paraccel. They have to hope that the exposure provided by Amazon will turn into on-premise business for them. They are still a venture-funded small company who has to compete against bigger players with larger sales forces. It will be tough.

My Guess at the Future

I worry about Vertica in the long run.

Until the Amazon deal I would have guessed that Paraccel was done… again, not because their technology was bad… it is not… but because it was not good enough to create a company that could go public and there was no apparent buyer… no exit. The Amazon Redshift deal may provide an exit. We will see? Maybe Amazon can take this solid technology into the cloud and make it a winner?

Since my blogs tend to be in response to some stimulus they may not reflect a holistic view on any particular product. The “My 2 Cents” series will try to provide a broader view…

From a technical perspective, Greenplum is my favorite data warehouse database. Built on the same architecture as Teradata (see here), the Greenplum team was able to extend the core of Postgres… first building out a shared-nothing architecture and then adding feature after feature… putting the heat on the other major players. Greenplum was the first row-based RDBMS to add full columnar support… and their data-loading capability is second-to-none.

Oddly they do not want to be in the data warehouse space. Their recent announcement (here) does not include any reference to data warehousing or business intelligence. The tweets from @Greenplum, the Greenplum website, and all things marketing are focussed on analytics and/or Hadoop. Even their page on data warehousing (here) has no articles on data warehousing. It is just not their target market. That is fine… the product is still a great EDW platform… but it is a worry.

Where They Win

The reason they target analytics is because they excel there. If your warehouse workload clogs because of big, complex, queries… Greenplum can win the day. Their data flow architecture, which keeps tuples moving from execution step to execution step without writing to spool provides them with the ability to beat the competition on analytics. They provide a very rich set of in-database analytics and some add-on capabilities to improve the productivity of your data scientist team.

Their data load architecture, which they call scatter-gather, is a big differentiator. If your problem is that you cannot get data loaded and reports out in your nightly batch window then the combination of scatter-gather and the ability to run big report queries is unbeatable.

Greenplum also has a unique solution for near-real-time. They marry Gemfire, an in-memory object-oriented database, with scatter-gather to move small batches of inserted data to Greenplum with a very small time delta. I do not believe this solution supports inserts or deletes as they have to be applied directly to the Greenplum database… but it is a nice capability for a certain class of problems.

Where They Lose

Greenplum, like Teradata, can be beat when the problem to be solved is narrow. In these cases, when the database supports a single application with a small number of queries or when it supports a narrowly focussed data mart, they are vulnerable to Netezza, Vertica, or even Exadata. It is also sometimes the case that a poorly designed POC can narrow the scope enough that Greenplum loses.

Greenplum can also lose when a full EDW is required. The basic architecture of the RDBMS is capable of supporting an EDW… but some of the operational features required… RASR, workload, incremental backup, etc. are not mature. This may well be the intentional result of their focus away from these features at analytics.

In the Market

Despite the worries Greenplum should be included in every POC. They will push Teradata hard in performance and in price/performance.

As noted here… I do not understand their market strategy. It seems that they are competing with themselves by offering Hadoop for analytics… but this cannot be a bad thing for customers even if it is an odd position in the market. The analytics market they favor is tough… relatively small (compared to the DW space)… emerging… there are several capable competitors… and the market is haunted by the same problem that killed the data mining market in the mid-1990’s… there are just not enough skilled data scientists (see here).

My Guess at the Future

I cannot guess at the future of Greenplum… They are being moved into a new business unit that could be spun into a new company that has a charter to build software for the cloud (see here). This is odd in several dimensions. First, as I noted here, the shared nothing architecture Greenplum is built on is not a perfect fit for the cloud. There are ways to get around this (maybe the topic for a future post?) but it will require development in a fundamentally new direction. Further, the new division seems to be a software-only venture. This makes the future of the EMC Greenplum Data Computing Appliance uncertain. I suppose that there will be announcements soon to clarify these questions… but the architectural disconnects make it likely that there will be some arm-waving for a while.

The TwinFin Surf Board (Photo credit: tvanhoosear)

Since my blogs tend to be in response to some stimulus they may not reflect a holistic view on any particular product. The “My 2 Cents” series will try to provide a broader view…

Netezza put a new spin on data warehousing… they made it easy. The Netezza software includes a unique clustered index feature called a zone map that is powerful and easy to use. They also use a FPGA co-processor to augment the CPUs, offloading data compression and projection. When both of these innovations combine Netezza is hard to beat.

Zone maps are powerful when they can be used in a query plan… but the hardware is only good, not great, when zone maps are not in the plan. FPGAs provided a huge boost when Netezza first came on the scene… but as discussed here they do not provide the same boost today. In addition, FPGAs may limit the ability of a Netezza cluster to handle concurrent queries (see here and especially the comments).

The IBM acquisition has opened up a market of Blue shops to Netezza… so they are selling… and as a result Netezza is here to stay.

Where They Win

Of course, Netezza will win in all-Blue shops.

Netezza wins when there is a naturally sequenced field in each big table that is also used in the predicate for most queries. For example, if data is naturally in date/time sequence and every query has a date/time constraint then Netezza is hard to beat. This is the case most often for focussed data marts or single application databases… so look for Netezza for these sort of problems.

Netezza wins when there are a relatively small number of concurrent queries… and they can win when the queries are complex… as long as the zone map is in the plan.

Netezza can win when the POC is designed such that zone maps may be used in the POC… for example when the POC models only a single data load and the data is pre-sorted… even when the real application would fragment the data (for example… data will not naturally enter the warehouse sequentially by customer number… the same customer will be represented time and again… but if you load once only for a POC then you can sort by customer number and use it in the query predicates).

Note that I am not saying that Netezza is a poor performer when zone maps are not used… it is good… but they would never win a POC if no queries used the zone map.

Where They Lose

Guess what? Netezza loses when the zone maps cannot be used or can be used for only a small fraction of the query workload. Note again that the use of a zone map depends on two factors: the data has to be in sequence over all time, and the queries must use the columns mapped in the predicate. If data enters the system out of sequence then the zone map fragments and eventually loses the ability to speed up queries (a few random out of sequence rows are OK).

This constraint makes it hard for Netezza to service data warehouses where, by definition, lots of different user constituencies come at the data from lots of different directions… rather than always using the path grooved with a zone map.

Netezza was designed when only Sybase IQ had columnar oriented tables… today columnar is in nearly every DW database and this allowed the competition to cut deeply into Netezza’s competitive, zone-map enabled, edge. Teradata columns, Greenplum columns, or the natural column stores can win even when zone maps are on target.

Bottom line: do a POC…

In the Market

I spend most of my time in the general market for data warehousing. You won’t see me offer much of an opinion on HANA for BW, for example… even though there are ten thousand plus BW warehouses I just do not see them in the places I work.

Before Netezza was acquired by IBM they were everywhere… in nearly every POC. Now… not so much. To a very large extent they seem to have been directed into the Blue-only customer base (now that I think about it the same thing happened to the Ascential Data Stage suite of ETL products).

My Guess at the Future

As I noted in the reference above… I think that Netezza will eventually go away from the co-processor strategy.

There have been rumors for several years of design that allowed multiple zone maps. This would be very important… but loading out-of-sequence data, which is the necessary the result, could be very slow.

Netezza has lost some of its edge as other technologies added columnar capabilities to their technologies… and Netezza is surely looking at this… but their architecture which includes an execution engine on the server and on the FPGA makes this more complex than you might suspect. Zone maps and two-stage optimization (one in the server and once in the FPGA) is cool… but a tight coupling of the tricks makes for a difficult time extending and adding new features.

If I were the King of Netezza and I could not find a reasonable way to extend beyond the two tricks that got me here I would go with the flow… I would position Netezza as an extremely easy-to-deploy data mart appliance and hook it tightly (i.e. build in some integration) along-side DB2 and Hadoop… and I would cede the EDW space to DB2 and the Big Data space to Hadoop.

Next up… my 2 Cents on Greenplum

May 1, 2013: Here is an update, or maybe a summary, of my view on Netezza… – Rob

If I were the Register I would have titled this: Raging Stuffed Elephant To Devour Two Warehouse Vendors… I love the Register… if you do not read it have a look…

This is a post is about the market implications of architecture…

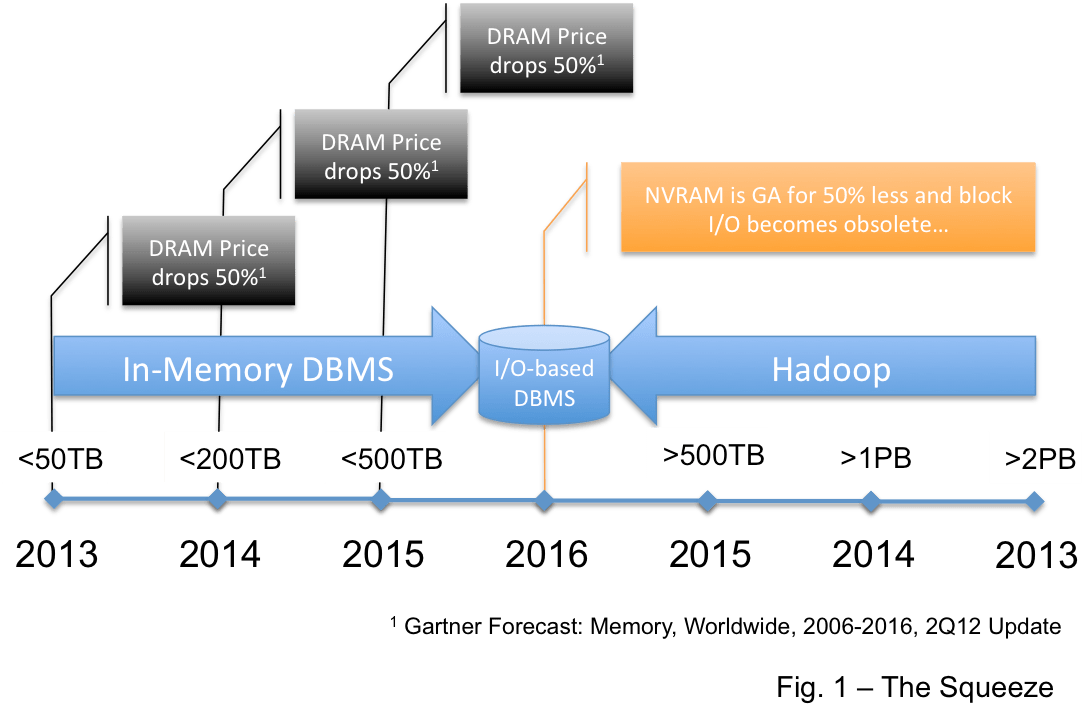

Let us assume that Hadoop matures and finds a permanent place in the market. This is not certain with some folks expressing concern (here) and others boundless enthusiasm (here). So let’s assume… and consider where it might fit.

One place is in the data warehouse market… This view says Hadoop replaces the DBMS for data warehouses. But the very mature BI/DW market requires a high level of operational integrity and Hadoop is not there yet… it is advancing rapidly as an enterprise platform and I believe it will get there… but it will be 3-4 years. This is the thinking I provided here that leads me to draw the picture in Figure 1.

It is not that I believe that Hadoop will consume the data warehouse market but I believe that very large EDW’s… those over 1PB… and maybe over 500TB will be compelled by the economics of “free” to move big warehouses to Hadoop. So Hadoop will likely move down into the EDW space from the top.

Another option suggests that Big Data will be a platform unto itself. In this view Hadoop will sit beside the existing BI/DW platform and feed that platform the results of queries that derive structure from unstructured data… and/or that aggregate Big Data into consumable chunks. This is where Hadoop sits today.

In data warehouse terms this positions Hadoop as a very large independent analytic data mart. Figure 2 depicts this. Note that an analytics data mart, and a Hadoop cluster, require far less in the way of operational infrastructure… they share very similar technical requirements.

This leads me to the point of this post… if Hadoop becomes a very large analytic data mart then where will Greenplum and Netezza fit in 2-3 years? Both vendors are positioning themselves in the analytic space… Greenplum almost exclusively so. Both vendors offer integrated Hadoop products… Greenplum offers the Greenplum database and Hadoop in the same hardware cluster (see here for their latest announcement)… Netezza provides a Hadoop connector (here). But if you believe in Hadoop… as both vendors ardently do… where do their databases fit in the analytics space once Hadoop matures and fully supports SQL? In the next 3-4 years what will these RDBMSs offer in the big data analytics space that will be compelling enough to make the configuration in Figure 3 attractive?

I know that today Hadoop cannot do all that either Netezza or Greenplum can do. I understand that Netezza has two positions in the market… as an analytic appliance and as a data mart appliance… so it may survive in the mart space. But the overlap of technical requirements between Hadoop and an analytic data mart… combined with the enormous human investment in Hadoop R&D, both in the core and in the eco-system… make me wonder about where “Big Data” analytic relational databases will fit?

Note that this is not a criticism of the Greenplum RDBMS. Greenplum is a very fine product, one of the best EDW platforms around. I’ll have more to say about it when I provide my 2 Cents… But if Figure 2 describes the end state for analytics in 2-3 years then where is the place for the Figure 3 architecture? If Figure 3 is the end state then I do not see where the line will be drawn between the analytic workload that requires Greenplum and that that will run on Hadoop? I barely can see it now… and I cannot see it at all in the near future.

Both EMC Greenplum and IBM seem to strongly believe in Hadoop… they must see the overlap in functionality and feel the market momentum of Hadoop. They must see, better than most, that Hadoop wins this battle.